There's a moment on the drive out of any Indian city when the landscape shifts. The malls thin out. The hoardings change languages. The ring road, the bypass, appears in your rearview mirror. We've spent the last 8 years driving past it and instead dwelling deep into these towns and have been early believers in the consumption story beyond the Top 25 cities. It is often debated whether we are investing in the wait or the inflection point? Is this patient capital or impact capital? Will the returns profile look different?

But here's what we've learned so far from actively investing in “Beyond the By-Pass plays” you can't copy-paste your way in. This is about choosing execution paths that match the market. The value market of Tier 2 & beyond is not underserved by Tier 1. The ~450 urban towns in India aren't a smaller version of the Top 25. They're not "Tier-1 five years ago." The trust curves differ. The infrastructure gaps differ. The GTM that works differs. The metrics that matter differ. The founders who win think differently.

The J-Curve of LVHV

Every investor knows the J-curve: value looks broken before it compounds.

Low-value, high-volume (LVHV) businesses behave the same way. On first inspection, they look wrong: low AOV, messy returns, thin contribution, accounting losses that scare anyone trained on metro playbooks. Then something flips. Cohorts mature. Logistics costs bend. Unit economics start compounding faster than complexity.

Last week, Meesho listed. The stock debuted at a premium and peaked intraday at ₹789B (~$8.8B). That wasn't "another consumer IPO." It was public markets underwriting an operating model built for India beyond the top metros, and paying up once the curve turns.

As a consumer investor with an active “Bharat-first” portfolio, I’ve observed in awe from the sidelines the outcomes that Meesho delivered for its earliest investors. We've been active early investors in Bharat-first businesses, CityMall, YellowMetal, Bimakavach, Chalo, Eloelo , and Meesho's successful IPO validates that the thesis scales. Geography is the opportunity, not the constraint.

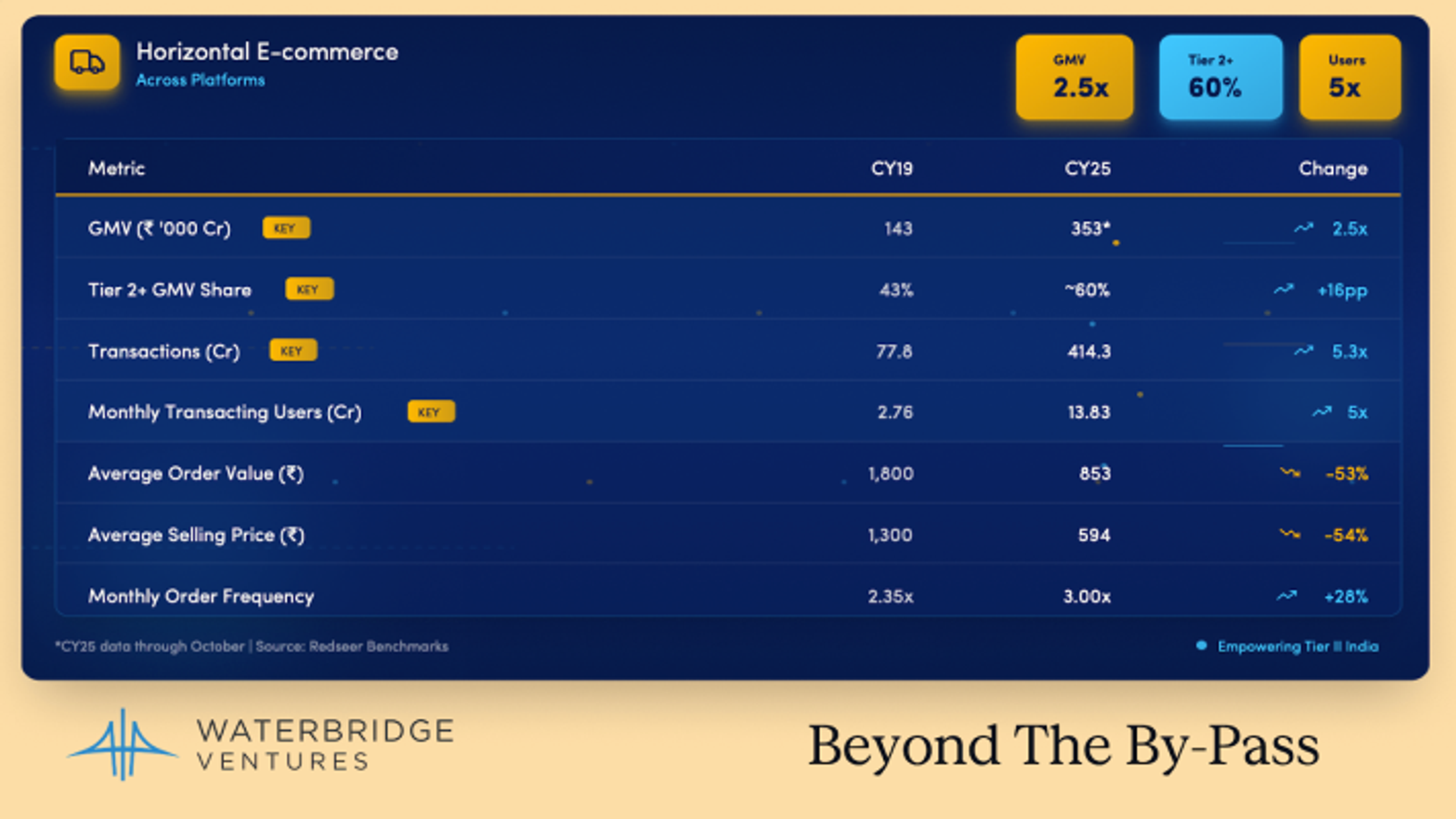

The Numbers That Pin the Story

India's horizontal e-commerce market tells a clear story. From CY19 to CY25, the structural shift is unmistakable:

Tier 2+ is now the majority. These markets went from 43% to 59% of horizontal e-commerce GMV in six years. In absolute terms, Tier 2+ GMV grew from ₹62,000 Cr to over ₹2,10,000 Cr, a 3.4× expansion while metros barely doubled. This isn't a secondary market anymore. It's the primary market. By 2030, tier 2 and tier 3 cities are expected to account for 65% of India’s total online shopping activity, compared to 35% for tier 1 cities, an inversion from the past decade.

AOV compression is structural, not promotional. Average order value dropped from ₹1,800 to ₹853, a 53% decline. Average selling price fell even more sharply, from ₹1,300 to ₹594. This isn't discounting. It's the market expanding into customer segments that transact at structurally lower price points. Affordability became architecture.

Frequency is the economic weapon. Monthly order frequency climbed from 2.35× to 3.00×, a 28% increase even as AOV compressed. When margins shrink per transaction, you survive on repeat. The platforms winning are those engineering habits, not event-driven shopping. Basket size stayed flat (~1.4 items), customers aren't bundling more, they're returning more often.

Transaction volume is the real story. Gross transactions scaled from 78 Cr to 414 Cr annually, 5.3× growth. Monthly transacting users grew 5× from 2.76 Cr to 13.83 Cr. The math: lower AOV × more users × more frequency = dramatically more transactions for comparable GMV growth.

That's LVHV math in action. Metro playbooks assume slack: higher AOV gives room for take-rate, experiments, and inefficiency while you learn.

At ₹500 AOV, slack disappears. Your margin for error isn't "a few percent", it's a few rupees. One return spike. One COD failure mode. One fraud vector. One support workflow that doesn't scale. Your contribution vanishes before the dashboard refreshes.

The LVHV Blueprint: Inertia → Infrastructure → Economics

Across commerce, credit, insurance, and mobility in Tier-2+ India, the same sequence keeps appearing. Miss a stage, and the model never stabilizes. Hit all three, and the J-curve appears.

Stage I: Inertia

The real competitor is status quo plus suspicion.

In Bharat markets, adoption dies before price becomes the argument. Consideration time runs longer. Before "price," users ask three questions:

- Do I understand what this is?

- Will I get cheated?

- Is anyone like me doing this?

Trust becomes distribution, not metaphorically, but mechanically.

At BimaKavach, insurance penetration requires building knowledge first; most customers don't know the fine print of what they're buying and mis-selling is rampant. At Eloelo, the "nearby" feature became most-used: users could see hosts streaming from their own city. A digital product, why should geography matter? But it did.

If the GTM doesn't explicitly hone and imbibe trust, CAC math becomes fiction.

Stage II: Infrastructure

You don't plug into rails. You become the rails.

Metro businesses stitch together best-in-class vendors and APIs. LVHV businesses can't. Every integration leak is a rupee leak. And rupees are the whole margin.

YellowMetal built branch-led infrastructure with their own LMS and feet-on-street sales managers. CityMall uses micro-entrepreneurs for last-mile delivery, a 2-3 year ramp you can't shortcut with digital marketing. Eloelo engineered low-latency streaming for ₹5,000 devices.

Infrastructure is why LVHV moats look "boring." They don't demo well. They compound.

Stage III: Economics or "Bharat-nomics" rather

Margin-per-transaction obsession fails. The sentence that separates tourists from believers: Optimize for contribution margin per customer cohort and lifetime value, not margin per transaction.

CAC/LTV paybacks will stretch longer than Tier-1 playbooks. It won't be a one-year payback. But once cohorts settle, they're loyal. Retention and repeat become the entire game.

Investor DNA that wins - evaluating LVHV Differently

Seeking Habit Formation

Unlike platforms deriving ~50% of GMV from annual sale events, LVHV businesses don't believe in Great Indian Festivals or Big Billion Days. Everyday low prices. Habit formation over spikes. The climb in order frequency in the table above from 2.35× to 3.00× is evidence: these aren't promotional bursts, they're behavioural shifts. At the early stage, what signals give evidence that the inertia problem described above is being addressed?

Profitability Despite Losses

LVHV platforms can be functionally profitable at the contribution level and free cash flow positive while showing P&L losses. Meesho's FY25 numbers make this concrete: Contribution Margin (Marketplace) of ₹1,484 Cr, free cash flow of ₹591 Cr, up 3× from ₹200 Cr the prior year, even with accounting losses. P&L reflects sequencing and accounting treatment. Cash and cohort contribution reflect physics. We are seeing a similar trajectory and patterns across CityMall and Eloelo as well. This forces a philosophical shift: evaluate long-term free cash per share, not accounting EBITDA.

Delayed Monetization

At a ~₹500 ASP, standard monetization assumptions break. Profit pools need to emerge from the supply chain and need to be multi-modal. Seller/Vendor services (fulfilment, tooling), Advertising (only if it doesn't degrade trust), Data, insights, and workflow economics, Embedded financial services (when rails exist). Monetization becomes an innovation problem, not a pricing problem. In LVHV, it must obey two rules: it cannot introduce uncertainty (or you lose trust and repeat), and it must improve the system (or you're taxing the engine you need to compound). Differently put, we need to monetize both sides of the platform, the demand side and the supply side.

The sequence matters: trust → repeat → monetization. This often means, as early-stage investors, we will see 12-24 months with no revenue. Do we, as investors, have the DNA for that?

Founder DNA That Wins

Platitudes are useless here. LVHV requires observable instincts, a specific kind of founder and a specific kind of organization.

Cost Discipline as Religion

Costs must scale sub-linearly with volume or the model collapses. Capital efficiency isn't a virtue; it's survival. What's the signature of a system learning to compound without buying every order?

The tell: Founders speak about cost like oxygen, not weather. It's not a quarterly commentary, it's a daily obsession.

The test: What cost lines bend with scale, and which don't, and why? If a founder can't answer with specificity, they haven't internalized the mechanics.

Trust-First GTM

Community, social proof, local credibility, assisted flows, predictable refunds, these beat brand advertising at the start of the Bharat J curve. Relationship-based sales, not digital-first acquisition.

The tell: Founders name the top reasons for second-purchase failure without looking at a chart. They know trust barriers because they've felt them.

The test: Can they show trust metrics improving by cohort, not just "NPS up"? Trust isn't a survey; it's repeat behaviour by geography and channel.

Deep Closeness to Market

Primary insights and innate understanding of the customer matter more than pedigree. Nikhil of YellowMetal is based in Chintamani. Bimakavach operates out of Indore. Chalo wants people who grew up travelling in buses, who come from that context, who understand the customer in their bones.

The tell: Founders talk in cohorts by default and describe customer behaviour without pulling up data. The market lives in their head.

The test: Where are they based? Who do they hire? How do they spend their time? Proximity isn't symbolic; it's operational.

Deep Tech Stack as Margin

AI personalization, multimodal search, automated seller tooling, fraud detection, address parsing, route optimization, these aren't "ML flex." They're margin protection at low AOV. Technology enables scale at low cost.

At Meesho, ~73% of placed orders come from feed and recommendation systems. That's not nice personalization, it's conversion insurance when users can't describe what they want in a clean taxonomy. Voice, text, and image search in 11 languages isn't a feature; it's the difference between a customer converting and a customer leaving.

The tell: Tech roadmap ties to specific CM leaks, not feature bragging.

The test: "Which 3 workflows did automation make cheaper, and by how much?" If the answer is vague, the tech isn't doing the work.

Organizational Culture That Compounds

LVHV demands a specific culture, one that mirrors the business model's constraints:

- Frugality as identity. Not performative cost-cutting, but genuine discomfort with waste. The culture should make expensive decisions feel wrong, not just financially, but morally.

- Customer proximity at every level. Not just founders, the entire organization maintains direct lines to customer reality. Engineers know what breaks. PMs know what confuses. Leadership knows what builds trust.

- Long-term orientation in hiring. LVHV companies can't afford mercenaries optimizing for 18-month cycles. They need believers who understand the J-curve rewards patience.

- Execution speed with quality. At low margins, you can't iterate expensively. The culture must enable fast, cheap experimentation: ship quickly, learn quickly, kill quickly.

Where This Points Next for us?

The Meesho IPO is a timestamp, paving the way for much larger opportunities ahead. We see three white spaces where LVHV physics will keep appearing:

LVHV Financial Services

Small-ticket, high-frequency credit, insurance, and investment behaviours won't be won with metro UX and metro underwriting assumptions. Trust rails, infrastructure rails, and cohort economics will dominate. The ₹5,000 loan. The ₹200/month insurance premium. The ₹500 SIP. These are different products requiring different operating systems.

LVHV B2B for Small Operators

Same inertia. Same need to become the rails. Same requirement to underwrite repeat and retention rather than one-time "activation." The 12 million kiranas aren't going digital because of a sleek app; they're going digital because someone solved working capital, delivery reliability, and trust.

Creator and Community-Led Vertical Commerce

Trust comes pre-loaded in relationships. Distribution can run cheaper. But the system still has to handle the messy reality, returns, COD, language, support, without breaking unit economics.

In Conclusion:

The data now says what we've believed for years: 5× more users, 5× more transactions, AOV halved, Tier 2+ now 59% of GMV, frequency climbing. The market has moved.

The blueprint is legible:

Trust before distribution. Rails before scale. Cohorts before vanity. Cash before optics.

The J-curve is turning. We're looking for the founders building the next operating systems underneath it. Write to Baba Prasad Nath Raj Nayan Datta or myself at WaterBridge Ventures and we look forward to speaking with you.